Intel Corporation (NASDAQ:INTC) was just named Citi Research’s top pick within the semiconductor industry. In a note to clients, analyst Christopher Danely ratcheted INTC up a couple of notches in Citi’s hierarchy and reiterated its “Buy” rating.

Those who know the Intel story well likely know why it’s a surprising call. Intel stock isn’t particularly well-loved by the analyst community right now. Plus, the echoes of the Spectre/Meltdown gaffe are still ringing. Throw in the fact that the PC market remains lethargic and that other players besides rival Advanced Micro Devices, Inc. (NASDAQ:AMD) are starting to design their own CPUs, and the future becomes even less compelling for Intel.

When one takes a step back and looks at the bigger picture though (as Danely has), the bullish table-pounding makes a lot of sense.

That’s What He Said…

Hockey legend Wayne Gretzky attributes his greatness to one overarching idea: “Skate to where the puck is going, not where it has been.”

It’s a valid point even for investors — you want to own (or not own) stocks for where they’re going rather than where they’ve been.

To that end, Danely explained of Citi’s bullishness:

“We believe the recovery in the enterprise end market will drive Consensus estimates higher on Intel as the enterprise end market is over 50% of Intel sales and has declined every year for the past three years. The enterprise end market drove upside to Intel in 4Q17 and we believe it will be sustainable in 2018 driven by the improving economy and increased spending from tax reform.”

Danely went on to call INTC its Micron Technology, Inc. (NASDAQ:MU) of 2018, when that memory maker’s stock almost doubled in value following an unexpected explosion in demand for computer memory. Specifically, he noted “We believe Intel is the only semiconductor stock with both poor sentiment and substantial upside to Consensus estimates. As a result, we are moving Intel from #3 to #1 in our company rankings.”

And that may be the only explanation that prospective owners of Intel stock can truly embrace.

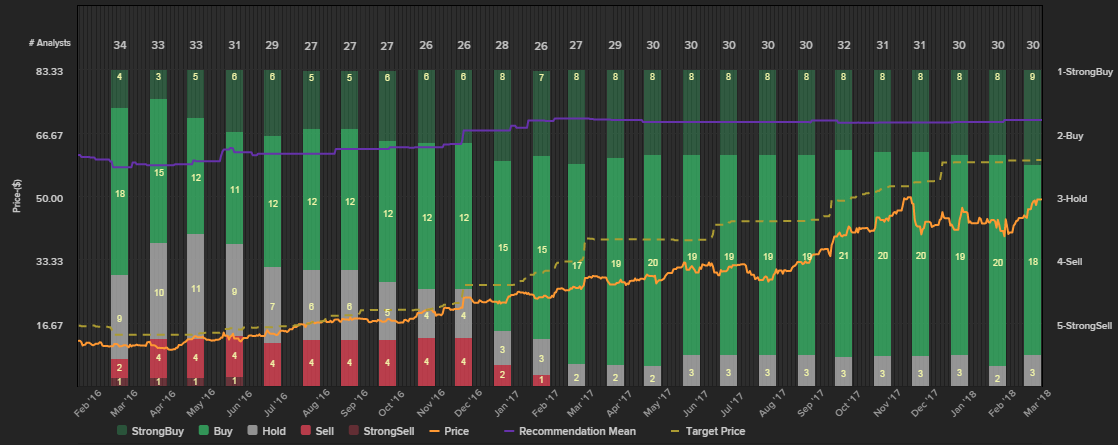

INTC Now vs. MU Then

Click to Enlarge

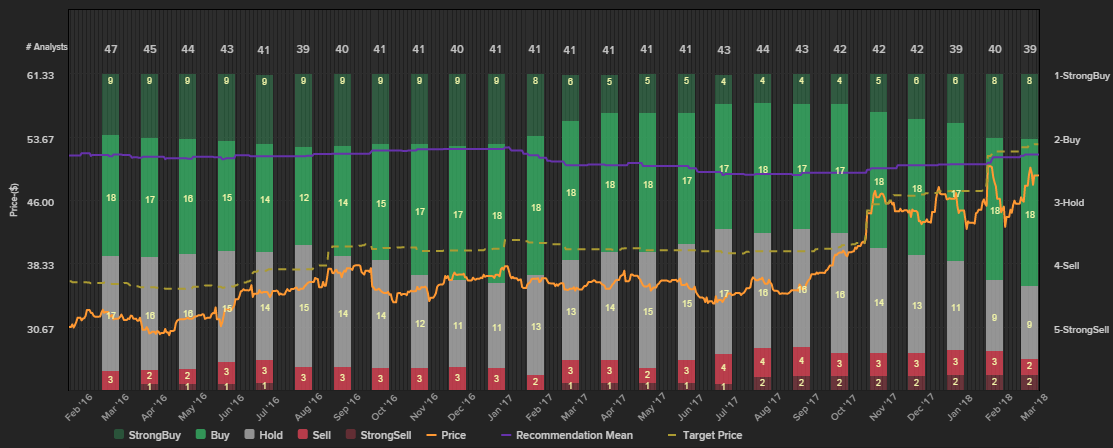

Compare the chart above, to Intel’s now (below).

Analysts collectively rate Intel shares at less than a “Buy” right now, leaning towards “Hold,” and as a group say Intel stock is only worth $52.69. That’s a mere 5.9% better than the stock’s current price, and by bullishly-biased analyst standards is practically a bearish opinion.

If Intel’s story unfurls like Micron’s, INTC may well be one of 2018’s Cinderella stories — and the pros will be forced to change their tune. In fact, the opinions are already starting to improve. Now that the ball’s rolling, momentum is likely to keep that ball rolling.

Click to Enlarge

To that end, Gartner’s 2018 forecast calls for a 4.5% increase on IT spending. It’s not a lot in absolute terms, but a great deal of growth when talking about an entire industry. Intel is well positioned to capitalize on that rising tide.

Industry Insider Offers Up Reality Check

But what about increasing competition for Intel? Primarily in the form of AMD’s deeper dive into the CPU market with its new Ryzen lineup?

Dell EMC’s Chief Technology Officer John Roese (who would know as much as anybody would on the matter) made things very clear last week, saying:

“Intel is the big player, AMD is the second player. There’s enough diversity between them that there are use cases to have them both in our portfolio, but just the sheer breadth of the Intel processor portfolio is massive compared to even the accelerated AMD world.”

Roese goes on to say:

“AMD is doing some interesting things, and by adding them to the portfolio we pick up a few extra areas, but let’s be very clear: there is a huge, dominant player in compute semiconductors, and then there is a challenger which is doing some very good innovative work called AMD, but the gap between them is quite large in terms of market share and use-cases. So our portfolio is not going to change in any meaningful way.”

Roese’s comments are likely more about the PC market than the data center market, but the data center market is even more for Intel’s taking than AMD’s.

In this light, Citi’s defiant bullishness actually makes plenty of sense.

Bottom Line for INTC Stock

As bullish as Danely may be, there’s no denying INTC stock has a bit of a valuation problem. The trailing P/E of 25 is a bit rich — even by technology stock standards. Despite the more palatable forward-looking P/E of 13.09, that’s likely to be a potential headwind eventually.

Valuation isn’t a huge problem just yet though. As, our very own Bret Kenwell pointed out just last week, Intel shares are on the verge of a bullish breakout. His argument holds water, even if he’s only looking for a short-term swing.

Regardless, when and if Intel stock finally dishes out a decent-sized pullback, that is a buying opportunity.

Not only is the forward-minded, value-based argument for Intel pretty solid, it’s very likely many of the doubting analysts are going to gradually make their way into the bullish camp. That’s going to set the stage for a quick end to any pullback that takes shape from here. And that string of upgrades would only fan the longer-term bullish flames.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.