Apple nabs parental controls patent for 'iWallet' transactions

Mikey Campbell

Mikey Campbell

The new patent, titled "Parental Controls," essentially establishes a set of guidelines which governs how users complete mobile electronic transactions and tightens security for device owners who have multiple accounts linked to a product or set of products.

Since 2010, Apple has filed a series of so-called "iWallet" patents that deal with mobile device payments including NFC systems that are linked to credit and debit accounts. The new rules would dictate how these transactions are made and by whom, thus allowing for tight control of finances for end users of the patented technology.

From the patent summary:

A method, comprising: defining one or more rules using a handheld electronic device, wherein the one or more rules establish restrictions on transactions made using a financial account associated with an account holder other than the user of the handheld electronic device; and applying the one or more rules to the financial account.

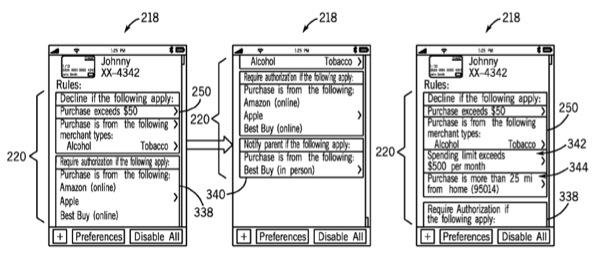

Integral to the patent is the definition of primary and subsidiary account holders, for example a parent and their child. In this model, the system would allow the parent to control their child's mobile transactions by setting predetermined limits that can then be transmitted to a designated financial institution that manages the subsidiary account.

Limits can be based on transaction amounts, spending over a given period of time and location, among other variables, giving the primary account holder a great deal of flexibility in restricting a subsidiary account. Although an iPhone was not specifically listed as the "handheld electronic device," the handset would be able to offer the data connectivity, geo-location data and processing functionality Apple is looking for in order to implement the control system.

Example of subsidiary account restrictions for mobile transactions.

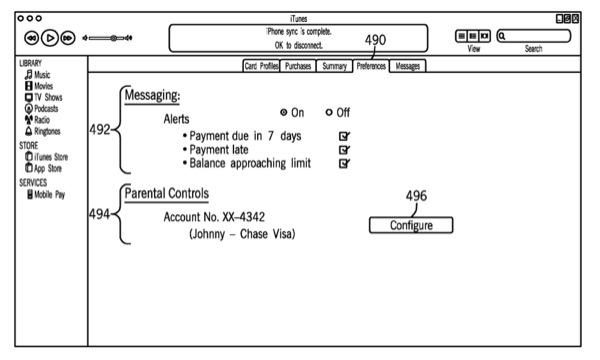

Of particular note are illustrations included in the patent filing that show iTunes acting as the hub through which transaction and financial information is passed. The tie-in would give Apple's extremely popular online media store the power to field real world transactions.

iTunes could be the hub of Apple's "iWallet" solution.

Advancements in Near Field Communication (NFC) and the gradual market shift away from cash has sparked an interest for tech companies to create so-called virtual wallets that allow users to pay with mobile devices instead of cash or credit cards.

Current NFC chips leverage RFID technology to either exchange data between two mobile devices that are in close proximity to each other, or read data from unpowered RFID chips. Google Wallet and Isis are examples of NFC payment systems, though though the former has yet to gain traction while the latter is expected to see release on select handsets this summer.

Apple's proposed system can be thought of as a more robust version of contactless payment solutions like those used in some major credit cards like MasterCard's PayPass.

Recently, the credit giant acknowledged that Apple could be a key player in bringing NFC tech into the mainstream due to iTunes' massive installed customer base, though the Cupertino, Calif., company has yet to utilize any of its "iWallet" patents.

Malcolm Owen

Malcolm Owen

William Gallagher

William Gallagher

Charles Martin

Charles Martin

Andrew Orr

Andrew Orr

Amber Neely

Amber Neely

17 Comments

Ah, they'll want to make iTunes get hacked less often before I ever commit to using it for that purpose.

4096-bit RSA encryption ought to do it.

With the requisite 30% service fee?

I'm not even sure I care about NFC anymore.

I've had something for years:

- a plastic card

- accepted everywhere

- easily replaceable if I lose it

Debit Card!

Ah, they'll want to make iTunes get hacked less often before I ever commit to using it for that purpose.

4096-bit RSA encryption ought to do it.

That's not why people get hacked. They get hacked because they use the same password with all their accounts, or someone is social engineering people at the Apple store. My CC has been on file with Apple for years. It's funny because I bought something from the apple store one day and they already had it on file.

With the requisite 30% service fee?

Maybe off the 1.75 to 3.75% transaction charge to the banks.

I think Apple's goal is to ultimately cut out the middle men. Just deal with Visa/MasterCard directly, not the banks.

Likewise with the mobile carriers, I think at some point you'll just get your wireless service from "Apple" that just runs on top whatever carrier is available like how Virgin Mobile already sells service in multiple countries without owning any local infrastructure.

The end game is that you can just buy everything from your iPhone/iPad/AppleTV/Mac, anywhere, anytime. Think of an example where you can ask Siri to find you a place to have a drink, inquire all the local drinking establishments who make it and their ratings, and then order/pay for the drink without having to get the attention of the server. That's one example that people can relate to. (Having to wait to get your order taken or payment.)

Imagine a world where your cellphone not only contains not only all your payment options, but also every form of ID imaginable, including your passport and other govt IDs. It connects to a web portal which you opt-in to that contains as much data as you can pump into it. For security, everything is protected by a 2-tier password (biometics, and a PIN).

That my friends is the promise of NFC. Convenience AND security. The only people that would need or want plastic are old farts resistant to change.