It hasn't been the greatest of times for shareholders of Apple (NASDAQ:AAPL). The high-flying tech name that shot up above $700 has dropped almost $200 in recent months. On Friday, Apple closed below $510, the lowest close since late February. Lately, a bunch of analysts have been taking down estimates or price targets on Apple, which has really caused the latest downturn. Some investors just saw Apple getting too high, and they took profits, as they saw $1,000 price targets completely unrealistic. Apple's latest earnings report put some fear into investors, as earnings and gross margin guidance surprised many. Apple doesn't feel indestructible anymore, but that doesn't mean the best days are behind the company. Apple can easily bounce back, but investors need to be reassured of some things. Here are some questions that Apple needs to answer over the next couple of quarters.

Are gross margins just returning to normal levels?

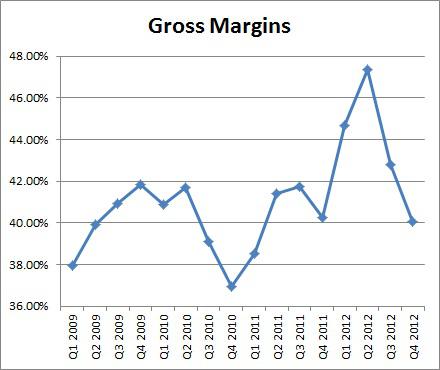

Apple seemed to shock everyone when it guided to just 36% gross margins for fiscal Q1, which is one of the main reasons the stock has taken such a hit. As you can see from the following chart, 36% gross margins would continue a recent downward trend, and would be lower than any single quarter over the last four years.

Now we all know that Apple is usually extremely conservative when it comes to guidance. So I'm guessing that most people think Apple will come in somewhere between 37% and 38% for fiscal Q1. Apple told us that this quarter will be the high end of the cost curve, because it launched so many products at once, and many of them have higher costs than previous products. Also, due to supply constraints, the company would incur extra transportation charges in an effort to get products to consumers quicker. It would seem logical that after fiscal Q1, margins would increase over the next couple of quarters.

In my opinion, Apple investors got spoiled thanks to the high margins of the iPhone 4S. Combine that with the fact that the phone released in October of 2011, so the phone's prime selling period lasted for fiscal Q1 and then Q2 as certain countries did not get the phone initially. The percentage of Apple's total revenue coming from the iPhone shot up, so Apple's margins did too. With the iPhone sales percentage coming back down, and Apple releasing so many new products, margins will come back down. Apple needs its iPhone sales percentage to be high. This could be the case if sales are really strong, and the China introduction appears to have gone well. More on this margin issue in the iPad section. For now, it just seems that Apple's gross margins are returning to "normal" levels, between 38% and 42%, which you can see is where the majority of quarters lie in the chart above.

What's going on with the regular iPad?

Apple might get some questions on how the regular iPad is doing. Going into Apple's latest report, analysts were expecting Apple to sell about 18 million iPads. Then, when Tim Cook gave a presentation just before the report, he mentioned that 100 million iPads had been sold. That forced most analysts to reduce their estimates to the 15-16 million range. Apple missed that number even, selling just 14.04 million in its fiscal fourth quarter.

Some were extremely surprised by the iPad miss, and many wondered if consumers were holding back purchases due to rumors that an iPad mini would be coming out soon. Well, Apple did announce an iPad mini in October, but it also announced a fourth-generation iPad, as it mentioned on the conference call. This was seen as a big surprise for many, who probably weren't expecting a new iPad to be released until March, as was the case with the iPad 3.

Lately, there's been a ton of analyst negativity regarding iPad numbers. The premise is that the iPad mini will significantly cannibalize regular iPad sales. Also, the mini seems to be supply constraint compared with the regular iPad. Mizuho Securities's Abhey Lamba was one of the first to talk about iPad numbers. She provided the following note in regards to her estimates.

Although iPad remains the market leader in the tablet space and it continues to solidify its number one position, the company's higher end tablet is being increasingly cannibalized by the lower end iPad mini. In our view, the iPad mini offers almost the same value as the larger iPad but is available for a significant discount, which is a big driver in the current macro environment and it also speaks to the price elasticity of the tablet market. As a result, we are also seeing an increasing demand for sub $200 tablets where Android is gaining share [...] Regarding iPad estimates, we believe current consensus of $11 billion for the December quarter (up 24% yearover-year) is too high. Assuming an ASP of about $450 (down 25% year-over-year), consensus iPad shipment forecast is around 25 million, which seems quite high given the lackluster demand being experienced by larger iPads. We are modeling iPad units to be around 20 million and ASP around $475. We believe the company is likely to deliver iPad revenues slightly below $10 billion for the quarter.

The next note came from Sterne Agee's Shaw Wu, one of the analysts I've cited numerous times in the past on Apple. Wu slightly increased his iPhone estimate for the quarter, but took down his iPad forecast from 25 million to 23.5 million, which made him take down his revenue forecast as well. He also referenced supply constraints for the mini, as well as cannibalization for the regular iPad.

NPD then came out with a note stating that Apple has more than doubled its iPad mini orders. It believes that the lighter and thinner model is hard to ignore for a significantly lower price, even if it has a lower resolution. The report states that the mini could represent half of all iPad shipments during 2013 if demand continues at the current pace. Separately, Digitimes is reporting that Apple is looking to enhance the resolution of the next iPad mini model that comes out.

Now the iPad mini is going to take down Apple's margins a bit. As Apple states in its conference call, "we priced it aggressively at $329, delivering incredible value to our customers. Its gross margin is significantly below the corporate average." But think about it this way as well. Even if the mini's margins were equal to the regular iPad, extra sales of the iPad in general mean the percentage of Apple's total revenue coming from the iPad is higher. That means that the percentage of revenue coming from higher-margin products, such as the iPhone, is lowered. Gross margins will come down, and as I showed in the section above, should return to "normal" levels. Part of Citi's recent downgrade was due to this iPad mini / regular iPad issue.

So Apple will need to address the regular iPad going forward. If the mini is so popular, will the regular iPad just go away? We should get an idea over the next couple of quarters whether the market is large enough for both products to exist successfully. If not, I wouldn't be surprised if the smaller version, today's "mini," eventually becomes just the "regular" version of the iPad.

What are you doing with the cash?

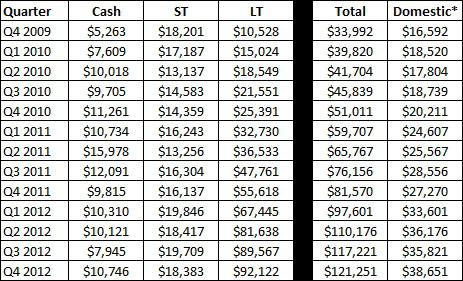

Apple investors have demanded in recent years that the company start returning some of its huge cash position to shareholders. The table below shows Apple's so-called "cash-pile," the collection of cash and equivalents, short-term investments, and long-term investments. Dollar values are in millions.

*Amount held within the United States, or cash not held by foreign subsidiaries. Numbers are close estimates, as Apple only provides foreign cash amount to nearest $100 million mark.

Now over the last three years, the total amount of cash and investments has risen by 256.70%. However, the domestic portion of that has only risen by about half of that, or 132.95%. As of Apple's latest quarter, less than a third, or 31.88%, of Apple's cash pile was held domestically. So when Apple shareholders see that Apple has over $121 billion in its cash pile, they have to realize that less than $40 billion is realistically available to the company.

Everyone knows that Apple announced a dividend and buyback in March. For those that forgot, here was the breakdown:

- $2.65 quarterly dividend starting in company's fourth quarter, or third calendar quarter.

- $10 billion buyback over three years, to start in company's first quarter of 2013, or fourth calendar quarter of 2012.

- Company expects to return $45 billion over three years, which also includes the remittance of withheld taxes related to net share settlement of restricted stock units.

When the company reports its fiscal first-quarter results, anticipated to be sometime in mid to late January, we will hear if the company did buy back any stock in the quarter. There are some that believe Apple will raise its dividend substantially in the coming months, but the cash position in the United States has not really soared since the original dividend announcement. I don't think Apple is going to raise it too much, my guess would be a raise to $3 per quarter, which would be a decent amount of growth. Remember, on the day Apple announced the dividend and buyback, it closed at $595.81. If Apple were to announce a raise to $3 per quarter today, the yield would be a great deal higher than the original yield due to the dividend raise and stock price decline.

Apple has not been a company to make large acquisitions, so those expecting Apple to use the cash for this purpose will be disappointed. Apple generally will only make small strategic acquisitions, whether it be a pool of patents, or a small company that can help an existing business or product line. Here's a list of Apple acquisitions over the years, and notice how the purchase price is never in the billions when the purchase price is given.

Many expect Apple's cash pile to rise into the $150 billion to $200 billion range over the next couple of years. But how much of that will be held domestically, $50 to $75 billion maybe? Investors are waiting to hear what Apple will do with its large cash position, and right now, the most logical uses are dividend raises and small acquisitions.

When does China Mobile (CHL) get the iPhone?

When it comes to Apple's next big source of revenue, there are two things everyone is looking for. First is the Apple TV that everyone seems to want. Rumors keep popping up here and there, but there hasn't been anything confirmed yet. But the second biggest item is when China Mobile gets the iPhone.

Deutsche Bank doesn't believe that a deal will be agreed upon anytime soon, for the following reason:

Deutsche Bank analysts said its recent meeting with China Mobile's management left them with the impression that there was little momentum for an agreement because of the "heavy subsidy burden" required to bundle the smartphone as part of its service offerings - an issue irksome to the Chinese government, which controls the company.

"We believe that the stars are not aligned for a China Mobile licensing of the iPhone 5," Deutsche Bank analysts said in a note. "The government is not supportive."

In its August operating update, China Mobile stated that it was up to 693 million subscribers, including more than 72 million 3G subscribers. If and when Apple could get a deal done, that would be an incredibly huge market for it to tap into. Currently, China Unicom (CHU) and China Telecom already have licensing deals with Apple, and they will have a head start on selling Apple's new phone.

Think about the numbers if a deal were to be completed. If Apple could get just 1% of China Mobile subscribers in the first year, that's 7 million iPhones. Imagine if it can get 2% of the total, or more. I think most people expect a deal to happen at some point, but when? There are still plenty of hurdles involved here.

Summary / Buy Recommendation:

Apple shares are at their lowest point in several months, and the stock was supported very well the last time it was close to these levels. While I'm not calling for a huge Q1 blowout right now, I think the fear in Apple will subside as margins rebound over the next few quarters. Right now, I think there is just too much fear around the name, which is why when you get one piece of bad news, the stock drops. Even if an analyst drops his or her price target from $780 to $700 right now, it shouldn't be a surprise, and it's not a reason to sell. The UBS analyst the other day put a $700 price target on a name trading at $530. That means that the analyst still sees a significant amount of upside.

Also, even if margins don't rebound to those 44% or 47% levels going forward, Apple is still an extremely profitable company. Apple's net income was over $41.7 billion in its latest fiscal year, and that figure could rise to $45 billion or more during this fiscal year. Huge net income numbers produce huge cash flow, and Apple will add to its tremendously large cash pile. Even with Apple having a large share of its cash outside of the U.S., it still has a sizable and growing domestic cash pile. That will allow Apple to buy back shares when they are cheap (like now at $510 as opposed to $700), as well as pay and increase the dividend. My current expectation is for Apple to pay its regular $2.65 dividend for 2 quarters in 2013, then raise it to $3 for the final 2 payments. That means investors would get $11.30 in dividends during 2013, which based on Friday's close, would be an annual yield of 2.22%. That's a pretty good dividend for a company that is expected to grow revenue around 25% this fiscal year (when you adjust for last year's 53-week period).

Additionally, investors are looking for Apple to eventually make a deal with China Mobile to sell the iPhone. China Mobile has nearly 700 million subscribers, so there is huge potential for Apple if a deal can be done. While a deal isn't coming this week, most probably expect one over the next couple of years. That would help spark the next leg of Apple's growth. Who knows what else Apple will do. Everyone expects a TV at some point, but Apple is certainly capable of surprising everyone. This is a company that has created some of the most innovative products in our history. Who expected the iPad, say seven years ago? I expect that creativity to continue. Apple was left for dead a couple of times, and proved everyone wrong.

Right now, there is an incredible amount of fear surrounding Apple, and that provides a unique opportunity for investors. Every time we get an estimate or price target cut, it makes shares cheaper for all. I'm sure a number of places are happy now that these negative notes keep coming out. Every time the price drops to $500, more people can back up the truck and purchase more. Those people aren't as prominent when shares are at $600. Don't forget, every time that an analyst cuts Apple estimates, it makes it easier for Apple to beat when it actually reports. Just look what happened last quarter. Without all of those late analyst cuts, Apple would have missed both estimates by a substantial margin.

In the end, those who believe in Apple should use this time to accumulate a position while shares are low. Last year around this time, I told investors to keep adding to their Apple position with shares under $400, and especially if we got under $375, which did occur a few times. Investors that used that fear around Apple as an opportunity were greatly rewarded. Apple has become more volatile this year, which has scared a lot away, but once the fear subsides, this stock is probably headed higher. Apple has some questions to answer, but what company doesn't?

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.